Improving CRA could help older tenants in the private rental market

01 Dec 2022

Life course changes associated with older age such as widowhood, disability and frailty suggest a need for a range of rental housing options. These include a private rental sector (PRS) that can support older tenants living in the general community, as well as options such as communal self-contained living spaces that provide some level of companionship, practical support and assistance with daily living, through to facilities that combine health care, personal care and accommodation.

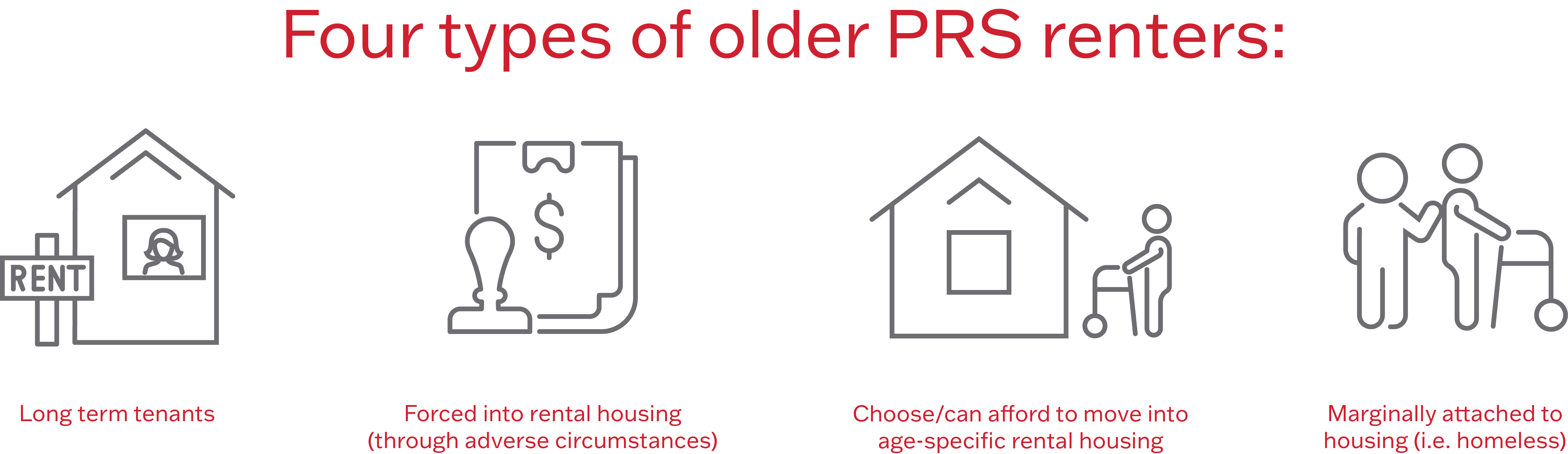

Housing policy options need to consider that there are four types of older PRS renters: some are long-term tenants; others are forced through adverse circumstances into rental housing (i.e. divorce, bereavement, financial circumstances); others choose / can afford to move into age-specific rental housing (e.g. resort style age housing); and some are marginally attached to housing (i.e. experiencing homelessness). Housing providers, including those in the PRS, must respond to this diversity of experience and preference.

Older renters – the key issues

Retired lower income households living in the PRS face rent increases and insecure tenure while being on low fixed incomes (i.e. the age pension). They also live in housing that may not be physically suitable for them and may require alterations to make the premises liveable (e.g. wider door openings to allow for wheelchairs, height adjustable kitchen benches etc.).

As tenants get older they are not be able to cope psychologically with stress and changes; may be suffering from physical disability and mental health concerns; may be frail and vulnerable; and can suffer from being isolated.

Finding housing solutions that are secure, affordable and appropriate to older renters is the key to keeping these tenants in their home and not being dependent on residential aged care.

Increasing Commonwealth Rent Assistance (CRA) for older tenants

Currently CRA is paid to an eligible ‘income unit’, which may be a household made up of a couple or an individual.

In the case of a household made up of a couple who both receive the age pension, if one partner dies (or leaves the relationship) the amount of age pension the surviving householder receives is effectively halved. However the amount of CRA the householder can receive is unchanged (i.e. the ‘economic unit’ is unchanged), meaning the person staying in the property has to continue to pay the same amount of rent as previously while receiving the same amount of CRA as previously but only have income from one age pension. As a result, rental costs now take up a significantly greater proportion of that individual’s income.

CRA could be restructured along the same lines as Housing Benefit in the UK, where there is a separate income test so that when a person suffers an abrupt reduction in income, Housing Benefit automatically increases up to a maximum of 100 per cent of the rent.

There are concerns such a reform will lead to work disincentives; however, for older tenants who are beyond retirement age these disincentives are of less concern. A separate income test for the over-65s would raise fewer concerns of this kind.

Such changes would be better targeted because older CRA recipients do not have an earnings profile to pay rising rents. The income tests can also be made sensitive to household type, so that they offer proportionately more support to singles, who often face greater financial hardship as they cannot benefit from the economies of scale in consumption that couples can.

Related resources

brief

brief

Rental brokerage officer to manage tenancies for older renters

Private rental brokerage programs (PRBPs) work with vulnerable households to access and sustain private rental tenancies through targeted early intervention assistance (e.g. advice, information, introductions and timely support) designed to build tenancy capacity and through building links with the local private rental industry so that they can compete successfully for rental properties in a competitive market and sustain their tenancies over the longer term. The programs help lower income tenants, including older tenants, who are less able to be successful in accessing housing in the market.

brief

brief

Head leasing for older renters

In head leasing, a housing agency (which could be a not-for-profit, for-profit or a government organisation) leases a property from a property owner and then on-leases the property to the tenant. The housing agency is responsible for making sure the landlord is paid rent at the correct time, that the property is treated with care and that leases, legalities and repairs are negotiated fairly with the landlord.

brief

brief

Programs to make home accessible for older tenants

Modifying dwellings to enable older residents to live more independently means people stay in their homes longer and saves governments money in not having to supply greater numbers of beds in supported age care establishments. However, for older people who do not own their dwellings such modifications are only possible with permission from landlords, and usually properties must be returned to their previous state when the tenancy ends. If the older tenant then has to move into another private rental dwelling they will have to pay for modifications (and repairs) again. This would be the case each time they are required to move into a new property.

Report

Report

Rental housing provision for lower-income older Australians

The number of people aged 65 years or over in low-income rental households will more than double by 2026.

Report

Report

The implications of loss of a partner for older private renters

This report aims to examine the effects of divorce, separation or bereavement on the housing and related financial circumstances of people aged 50 or over in different housing tenures, and in parti