Falling interest rates locked first home buyers out of the market

Extended periods of low interest rates can lock out first home buyers from the property market, according to new research from the Australian Housing and Urban Research Institute (AHURI).

18 May 2023

The study, ‘Financing first home ownership: modelling policy impacts at market and individual levels’, undertaken for AHURI by researchers from Curtin University, University of Sydney and RMIT University, modelled the relationships between different housing finance conditions and people’s ability to buy their first home.

Distinguished Professor Rachel Ong ViforJ from Curtin University’s School of Accounting, Economics and Finance is the research lead author, and says the lower interest rates have locked people out of the market.

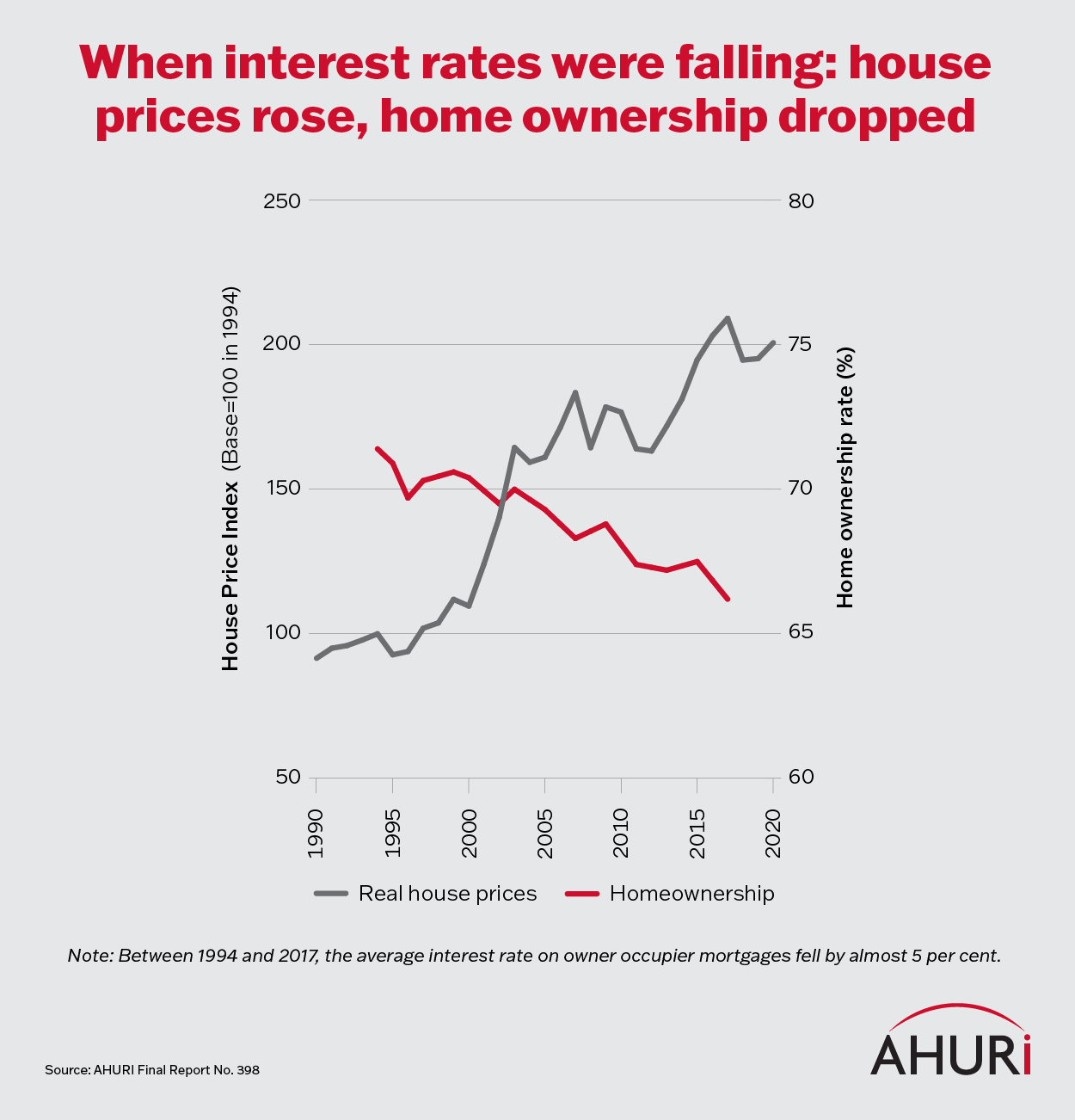

In the 25 year period between 1994 and 2017, the average interest rate on owner occupier mortgages fell by almost 5 per cent. As a result, demand for properties grew, and over this same period, house prices more than doubled.

The research found almost one-third of the price rises were caused by lower interest rates, with factors such as housing availability, wages and population growth accounting for the remaining increase.

‘Falling interest rates may seem appealing to first home buyers, but in real terms, it only increases competition and pushes prices higher, sometimes out of reach for those trying to get into the market for the first time,’ said Professor ViforJ.

According to the study, 84 per cent of aspiring first homebuyers do not have enough savings for a home deposit, with 71 per cent unable to meet the mortgage repayment requirements, preventing them from entering the housing market.

Nearly nine in ten aspiring first home buyers are locked out of home ownership due to borrowing constraints.

The research also notes that the housing market could see the return of young or lower income households again if a persistent rise in interest rates leads to a decline in house prices.

Help to Buy assists more first home buyers than the Home Guarantee scheme

Given the challenges first home buyers face in the current market, the study also modelled two first home buyer assistance programs to support home buyers on lower incomes: a mortgage guarantee scheme according to the design of the Home Guarantee scheme and a shared equity scheme modelled after the Help to Buy program.

The research found a mortgage guarantee scheme could assist 22 per cent of qualifying first home buyers, while a shared equity scheme would assist 41 percent of eligible home buyers, a quarter of which would be in the bottom 20 per cent of Australia’s socio-economic status areas.

‘Our research indicates that while both schemes will help some households into first home ownership, the Help to Buy shared equity scheme is likely to be more accessible to people on lower incomes than the Home Guarantee scheme,’ said Professor Ong ViforJ.

‘It’s important to understand that while these schemes would support people living in lower socio-economic status areas, they would likely also boost demand for housing in these entry-level markets,’ said Professor ViforJ.

‘It’s imperative the introduction of any such schemes is matched by an increase in the supply of local housing in order to avoid fuelling further house price rises.’

Read this report

Financing first home ownership: modelling policy impacts at market and individual levels